FUNDAMENTAL ANALYSIS OF STOCKS: PART 3. Balance Sheet

FUNDAMENTAL ANALYSIS OF STOCKS: PART 3. Balance Sheet

Continuing to explore financial statements, let's move on to the Balance Sheet.

In our research, we will use the Morningstar resource.

Unlike the Income Statement, which reveals the company's revenues and expenses, the Balance Sheet will reveal concepts such as assets, liabilities, equity, and debts.

To understand each line item, we must first understand what companies are composed of.

What companies are composed of: Balance, Capital

A group of people gathers initial capital through their own funds or borrowed money and issues shares of their company. These shares constitute equity. Essentially, this is the money of the organizers.

Next, by issuing shares or taking out a bank loan, shareholders create liabilities, which are divided into current (to be repaid within a year) and long-term (over a year).

By using borrowed money and equity, the company begins purchasing the assets

necessary for its effective operation.

Thus, we can say that Assets - Liabilities = Equity, just as Assets = Liabilities + Equity, and Liabilities = Assets - Equity.

Therefore, if a company lacks current assets to settle its current liabilities, it will have to use reserves from its equity. If a company’s long-term liabilities exceed its equity, it will have to work effectively to accumulate the necessary funds by the due date, or it will need to refinance its debt, which can negatively affect the company’s reputation.

After all the main activities: organizing debt, purchasing assets, selling products, paying expenses, and dividends (if any), the company can use the remaining funds in the following ways:

- It can allocate funds to retained earnings, thereby increasing equity and making the company more resilient to future shocks.

- The money can be used to pay down the principal of the debt, reducing future interest payments.

- Finally, the company can buy back its shares from the market (buyback) if it believes that the share price is undervalued and in the future it can sell shares to investors at a higher price.

Now, that we understand that assets are a derivative of equity, liabilities, and the company’s activities, and that equity is the difference between assets and liabilities, we can move on to reviewing each line of the balance sheet.

Detailed Company Balance Sheet

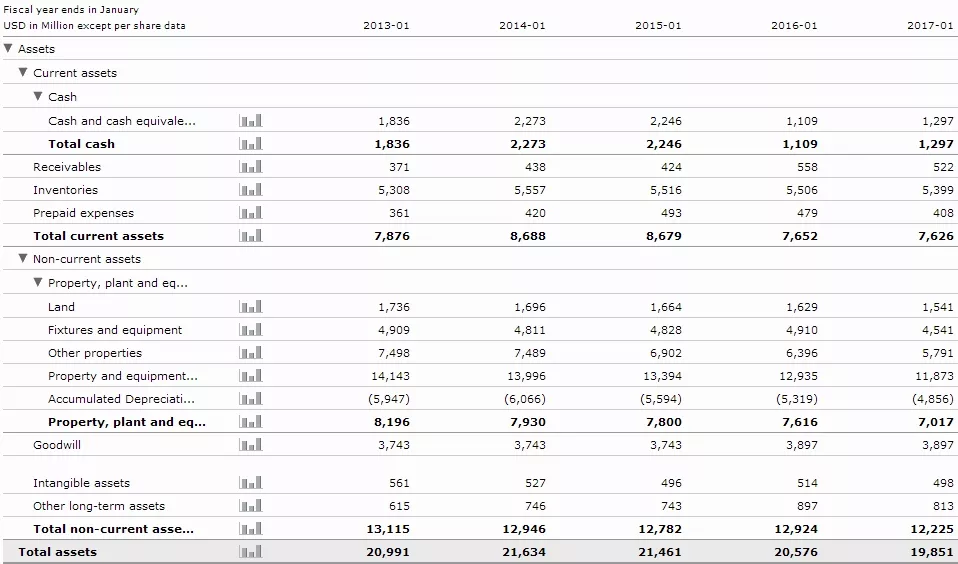

We start with Assets. The Current assets block (assets that are expected to be converted into cash within one year or less):

- Cash and cash equivalents – In addition to cash, this includes bank accounts, marketable securities, treasury bills, and short-term government bonds, i.e., anything that can be converted into cash in three months or less. Marketable securities are considered cash equivalents because they are liquid and not subject to significant price fluctuations. If the company operates in multiple currencies, this line will represent them as one based on conversion rates.

- Receivables – Debts owed to the company, rather than the company being the debtor. This arises when the company sells goods but has not yet received payment, often involving sales on credit. It’s important to note that even if the chance of repayment is low, Revenue in the Income Statement will still increase by the amount of the receivable, as Revenue collects even unpaid amounts. It is crucial to monitor the dynamics of this indicator. One simple way to analyze it quickly is by tracking the receivables in relation to Revenue. For example, Revenue/Receivables for Macy’s: 74.6, 63.7, 66.28, 48.52, 49.38. A sharp drop suggests a significant increase in credit sales, which may negatively affect future results due to potential bad debts. It is ideal when this ratio remains stable.

- Inventories – Raw materials, finished goods, and products ready for sale, all considered assets that are ready or will be ready for sale. Inventories are crucial as their turnover is a primary source of income and profits for shareholders. It is important to monitor inventories only if the company is making a profit on each sale. This line can be tracked through Revenue as Revenue/Inventories. For example: 5.21, 5.02, 5.09, 4.91, 4.77. A declining ratio indicates a slowing turnover of inventories.

- Prepaid expenses – For example, insurance is a prepaid expense because the purpose of purchasing insurance is to protect the company in case of future incidents. While this is an expense, it provides future benefits, much like prepayment for equipment.

- The Non-current assets block – assets that will take more than a year to convert.

Sub-block Property, plant and equipment (PP&E) – also known as tangible fixed assets. PP&E includes land, buildings, and vehicles. The sale of fixed assets is rarely a positive sign.

- Land – The term "land" includes all physical elements given by nature, such as fields, forests, minerals, and water sources.

- Fixtures and equipment – Tables, chairs, computers, electronics, bookshelves, partitions, and vehicles like trucks and tractors. All the equipment regularly used by the company falls into this category.

- Other properties – Anything that doesn’t fit into the categories mentioned above.

- Property and equipment, at cost – Includes buildings and major equipment like machinery and packaging equipment.

- Accumulated Depreciation – Essentially depreciation, with a small distinction that in the West, depreciation and amortization are separate concepts. Depreciation refers to the gradual expense recognition of an asset’s value as it is used. If an asset is bought and has a useful life of one year or less, its cost is immediately expensed. If the asset has a longer useful life, its cost decreases gradually until it reaches its minimum residual value. Depreciation allows companies to lower taxes as it is considered an expense, which forces businesses to continuously update PP&E so that they don’t rely on assets that have already depreciated.

- Goodwill – Intangible assets, such as brand value, a strong customer base, good employee relations, and patents. Goodwill is considered an intangible asset as it is not a physical item like buildings or equipment.

- Intangible assets – These assets are not physical in nature. Corporate intellectual property, including patents, trademarks, copyrights, and business methodologies, fall under intangible assets.

- Other long-term assets – Other long-term assets not classified elsewhere.

Detailed Review of Company Assets

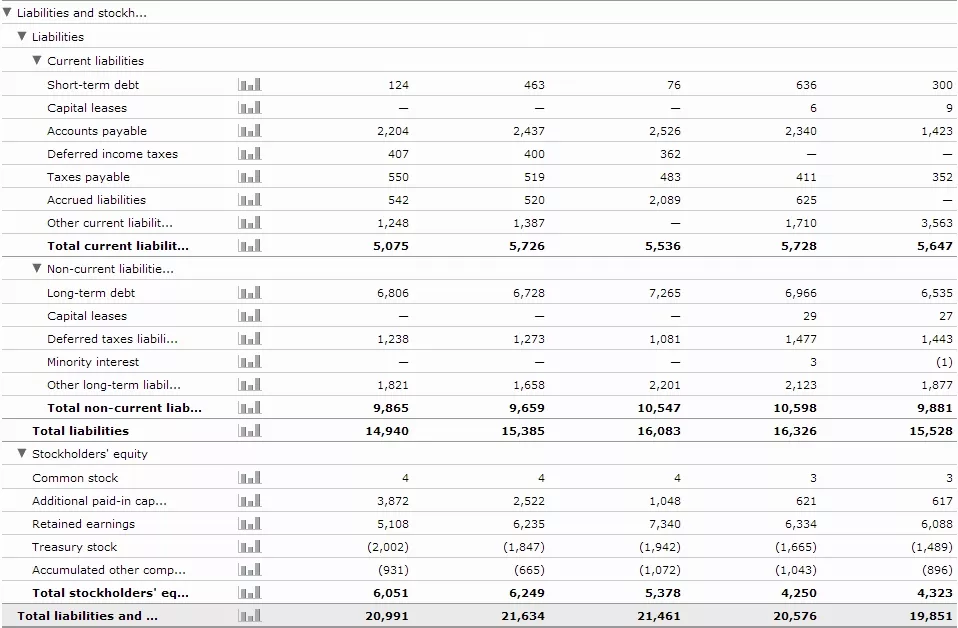

Now that we’ve completed the asset review, it's time to move on to liabilities and equity.

- Short-term debt – Short-term liabilities, including any financial obligations due within a 12-month period or within the current financial year, such as short-term bank loans and supplier debts. The value of ST Debt is important when determining the company’s financial health. If ST Debt exceeds the company’s cash equivalents, this suggests poor financial health and insufficient liquidity to cover short-term debts.

- Capital leases – Leases that meet certain criteria, including a lease term of 75% or more of the asset’s useful life, a purchase option at below-market value, and the lease value being more than 90% of the asset’s market value.

- Accounts payable – Debts owed to suppliers. It is often difficult to distinguish between short-term debt and payables.

- Deferred income taxes – Occurs due to differences in tax accounting and Generally Accepted Accounting Principles (GAAP), leading to situations where income taxes payable according to tax returns may differ from the expense reported on the income statement. This discrepancy is reflected in this item.

- Taxes payable – Taxes that are due to be paid within the year.

- Accrued liabilities – Payroll taxes, including social security, Medicare, and federal unemployment taxes, which have been accrued but not yet paid.

- Other current liabilities – Liabilities not included in the categories above.

- Long-term debt – Similar to short-term debt, but due in more than one year. This can be subdivided into financial liabilities (debts to investors or shareholders, including bonds) and operational liabilities (such as leases and pension plans).

At this level of review, this covers the long-term liabilities, as the remaining long-term liabilities have already been discussed. Let’s now conclude by reviewing Stockholders' equity.

- Common stock – This represents the initial nominal value established when the company was founded, usually multiplied by the number of shares issued. Therefore, this value tends to be low in this section.

- Additional paid-in capital – This appears after the company goes public through an IPO. The difference between the nominal value and the IPO price represents the company's profit from the IPO. It is often the company’s net gain, as the nominal value is arbitrary.

- Retained earnings – The final profit left in reserves after all operations, for reinvestment or repaying the company’s principal debt. It is calculated as the previous retained earnings plus net income minus dividends.

- Treasury stock – Shares not available for external investors, often representing the controlling stake. These are not included in the outstanding shares. Their number can increase through buybacks and decrease through offerings. Negative values here suggest a buyback.

- Accumulated other comprehensive income – Includes unrealized gains and losses from certain investments, pension plan profits and losses, and foreign currency transactions. OCI is excluded from net income since it involves non-recurring transactions.

As a result, the balance sheet’s total liabilities and stockholder’s equity will equal total assets, which we discussed at the beginning: Assets = Liabilities. This concludes our review of the Balance Sheet.

Recommendation – This text does not need to be memorized. It will come to you naturally. Practice makes perfect. When you’re studying stock fundamentals and balance sheets, the best practice is to not just read, but understand how to read balance sheets and translate your analysis into actionable insights.