Fundamental Stock Valuation: Part 2. Income Statement

Fundamental Stock Valuation: Part 2. Income Statement

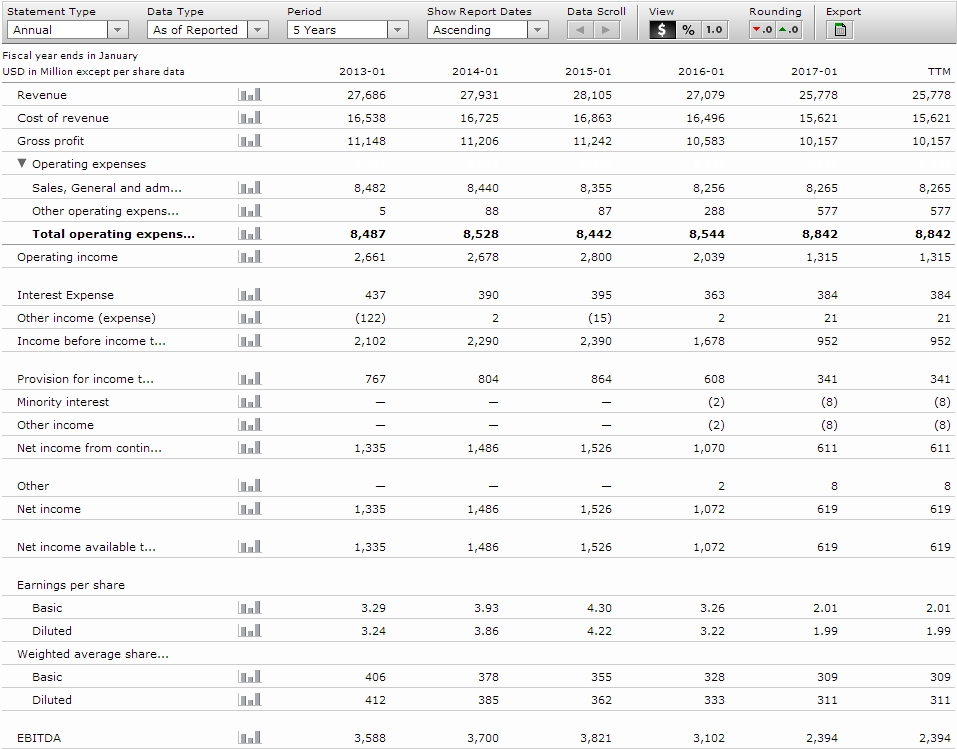

Continuing the series of articles on fundamental analysis, in this article, we will examine the Income Statement of Macy's Inc. (M).

Let's take a closer look at the Income Statement.

Income Statement | Fondexx

To understand what information can be extracted from it, you need to understand what each line represents. Let's break them down.

Revenue – the number of products multiplied by their price. That is, net sales, excluding any expenses. It is often called the Top Line because it appears at the very top of the statement. The dynamics of Revenue is more indicative than net income since it is harder to manipulate, but it has its nuances.

- It is important to remember that the company may include in Revenue products that have been paid for but not delivered yet, or products that have been delivered but not paid for yet (i.e., sales on credit).

- Revenue consists of operating revenue and non-operating revenue (income directly from the company's business and income from other activities). For example, income from the sale of assets, unforeseen expenses from investments, or money received from legal settlements would be considered non-operating revenue. Sometimes, this can significantly increase or decrease revenue.

- Of course, revenue should grow smoothly year over year, without significant volatility.

Cost of Revenue – includes all expenses necessary to produce the product. It includes marketing expenses, delivery to consumers, labor costs, fees, materials, sales discounts, and overhead expenses allocated to the product. The pure cost of production, i.e., the material costs for the product, is reflected in another section of the balance sheet - Cost of Goods Sold (COGS).

Gross Profit – essentially Revenue minus CoR, meaning how much the company earned after deducting primary expenses from total revenue. To evaluate it more objectively, it is useful to measure it as a percentage each year. That is, Gross Profit/Revenue*100. For our example, the dynamics are as follows (starting from 2013): 40%, 40%, 40%, 39%, 39.4%. As we can see, even in difficult times for the company (it has had a 3rd consecutive year of declining revenue), it tries to harmoniously reduce CoR while maintaining gross profit at around 40%.

Operating Expenses - abbreviated as OPEX, operating expenses include rent, equipment, inventory expenses, marketing, management salaries, insurance, and funds allocated for research and development. Let’s go through each of them.

Selling, General & Administrative Expense (SG&A) – all direct and indirect expenses related to sales and administrative activities. For example, the salary of management or costs associated with warranty services. These are often divided into direct (transportation, delivery, sales expenses), indirect (advertising and marketing of the product, phone bills, travel, and sales staff salaries), and administrative (including rent/mortgage for buildings, utilities, insurance, management salaries).

Other Operating Expenses – includes outsourcing costs, expenses for raw materials and supplies that cannot be stored in inventory (e.g., water, energy, small equipment, maintenance items, office supplies, etc.), repair and maintenance work, insurance premiums, research and development expenses, etc. These are expenses that did not fit into CoR or SG&A. Some companies may list part of the other operating expenses as external line items, so within the operating expenses section, R&D (research and development) may be included, though for other companies, it will be part of other operating expenses.

Operating Income – essentially Revenue minus CoR, minus Total Operating Expenses. That is, revenue minus cost of goods sold and administrative and operating expenses. Just like with Gross, we are interested in the dynamics in absolute terms and as a percentage change: 9.6%, 9.6%, 10%, 7.5%, 5.1%. As opposed to gross profit, we can see that the company is currently experiencing a sharp decline in operating income. Declining revenue, increasing other operating expenses, and difficulty reducing administrative expenses have led to a halving of operating income.

Interest Expense – the interest payable on any loans, bonds, convertible debt obligations, or credit lines. Interest Expense on the Income Statement represents the interest accrued during the reporting period, not the amount of interest paid during this period.

Other Income (Expense) – other income/expenses, including exchange rate differences and foreign currency fluctuations, bank charges, and other income and expenses.

Income Before Income Taxes – this is another intermediate figure on the way to net income. It is also recommended to measure it as a percentage to better understand the impact of interest on the company’s profit: 7.6%, 8.1%, 8.5%, 6.1%, 3.6%. The pre-tax profit has halved, which indicates that the burden of interest has not increased. We could say it increased if there had not been a similar 2x decline in operating income.

Provision for Income Taxes – the amount of taxes to be paid to the budget after the reporting period.

Minority Interest – minority shareholders are those who own less than 50% of the shares in the company. That is, they are shareholders but not major stakeholders. This line shows the portion of profits or losses attributable to minority shareholders in subsidiaries. For example, if a company holds 80% of a subsidiary and the subsidiary's profit is $100,000, then 20%, i.e., $20,000, will be listed as a loss for the minority shareholders. In our case, it’s 2 and 8 million dollars in favor of minority shareholders in 2016 and 2017.

Other Income (Other Income/Expense) – any other income and expenses that, according to regulations, could not be included in the higher lines of the balance sheet.

Net Income from Continuing Operations and Net Income – essentially the same thing; the differences between them will be discussed later, although these differences are very minor. Net Income is what is called the Bottom Line, as it appears at the very bottom of the Income Statement. From our example, we see that, like Revenue, the company's net income has been declining for 3 consecutive years. Let’s look at how this is reflected as a percentage: 4.8%, 5.3%, 5.5%, 3.9%, 2.4%. As we can observe, net income has halved, just like operating income. It is approaching zero. For the company’s stock price to soar, the company must at least forecast a recovery in this figure.

Earnings Per Share – net income divided by the total number of outstanding shares. This is the figure that is most often shown in the news and at the top of reports. The difference between Basic and Diluted is also worth considering later, as in reality, there are more than two types of EPS.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) – the formula is as follows: EBITDA = Net Profit + Interest + Taxes + Depreciation + Amortization. This is a relatively new figure and is often used to evaluate firms that are not currently making money but, if their projects succeed, the price of their stocks could soar. This typically applies to pharmaceutical and technology companies. Since this figure does not account for important expenses, it is often used as an accounting trick to "dress up" a company's profit and present it in a more favorable light.

With that, we conclude the initial breakdown of the Income Statement and will move on to the Balance Sheet next.