Fundamental Stock Valuation: Part 4. Cash Flow

Fundamental Stock Valuation: Part 4. Cash Flow

This is the 4th part of the introduction to fundamental analysis, focusing on the Cash Flow Statement. Earlier, we learned that the Income Statement shows whether a company is profitable and outlines its main expenses. The Balance Sheet revealed the structure of the company’s assets, liabilities, and equity. The Cash Flow Statement, however, provides a more detailed look at how exactly a company generates profit, how effective its core operations are, whether it reinvests in itself, repays its major debts, and if it has any leftover cash after all operations. Let's continue examining the company Macy's Inc.

Company's Financial Reporting in Detail

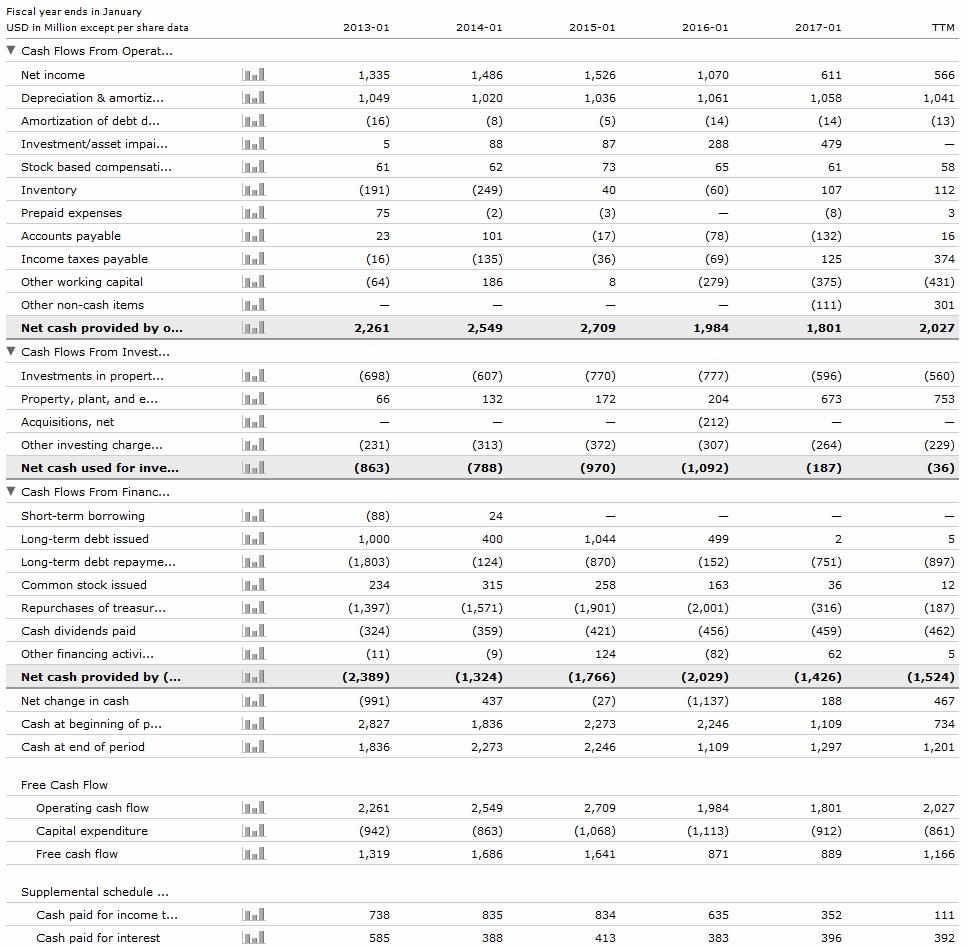

Block: Cash Flow from Operating Activities

This block reviews all cash flows directly related to the company’s core operations.

- Net Income — NI is calculated by subtracting business expenses like depreciation, interest, taxes, and other costs. This figure is typically used to calculate EPS (earnings per share).

- Depreciation & Amortization – As discussed previously in the Balance Sheet article, depreciation refers to the reduction in value of tangible assets, while amortization applies to intangible assets. For example, if XYZ Biotech spends 30M USD on a 15-year patent, the company would register 2M USD annually as amortization expenses over the patent's life.

- Amortization of Debt Discount/Premium and Issuance Costs – This includes expenses related to issuing debt, such as bonds, as well as amortization changes in debt payments.

- Investment/Asset Impairment Charges – This involves assets whose market value is lower than their stated value on the balance sheet. After adjusting the book value of the impaired assets, the loss is reported. Impairment should only be recognized if expected future cash flows are not recoverable. Even if the market value recovers, generally accepted accounting principles (GAAP) require the impaired asset to remain recorded at the adjusted value.

- Stock-Based Compensation – This refers to the use of stock options to reward employees. For example, an employee might be given the right to purchase 2000 shares at 20 USD each over 5 years. The right can be exercised after 3 years.

- Inventory – Inventory includes stock that does not account for future arrivals or shipments.

- Prepaid Expenses – These are assets created by payments for goods or services to be received in the near future.

- Accounts Payable – This refers to the debts owed by the company, including amounts due for goods or services already received.

- Income Taxes Payable – This refers to taxes owed to the government within the next year, calculated according to the current tax laws of the country in which the company operates.

- Other Working Capital – Working capital is the difference between current assets and current liabilities, which reflects the company's equity. In the Cash Flow statement, it shows the change during the period, excluding future accruals or write-offs.

- Other Non-Cash Items – These refer to changes in profits/losses that are merely accounting entries, not actual cash flows, such as adjustments to the balance sheet.

- Net Cash Provided by Operating Activities – This is the summary figure for all operating activities. It essentially replaces revenue, as operating activities only involve completed transactions, unlike revenue, which includes future events.

Next Block: Cash Flows from Investing Activities

This block includes cash flows related to the company's investments, such as purchases of other businesses.

- Investments in Property, Plant, and Equipment (PP&E) – As previously mentioned, fixed assets are subject to depreciation each year. Since depreciation reduces tax payments, companies need to continually replace equipment to maintain depreciation levels. This line shows how much the company invests in updating its fixed assets. Ideally, depreciation and PP&E investments should be closely aligned.

- Property, Plant, and Equipment Reductions – This refers to the sale of fixed assets, which usually brings in cash. Hence, this figure is often positive.

- Acquisitions, Net – This refers to the acquisition or partial purchase of another company, whether through vertical or horizontal integration. After an acquisition, the company typically requires time and additional expenses to fully integrate and align operations, often resulting in negative financial impacts in the short term.

- Other Investing Charges – This includes any other investment-related gains or expenses not captured in the previous lines. Depending on the industry, this can cover various investment sources.

The total in the Investing Activities section is often negative since investments generally represent outflows. If these investments are successful, they will gradually flow back into operating activities.

Cash Flows from Financing Activities

This block shows all cash flows related to new borrowings and repayments of existing debt.

- Short-Term Borrowing – These are all the company's short-term obligations, typically loans that need to be repaid within one year.

- Long-Term Borrowing – These refer to loans with repayment terms exceeding one year.

- Debt Repayments – This represents the actual repayment of debts, reducing liabilities.

- Other Financing Activities – This includes any other financial activities related to the company’s financing activities.

Cash Flows from Financing Activities (Continued)

- Dividends Paid – This is the portion of net profit that the company decides to distribute to its shareholders. For high-income companies, dividend payments are an important part of their financial strategy. Dividends can be paid regularly or as a one-time distribution and are usually made in cash. These operations reduce the company’s cash, thus representing an outflow in the cash flow statement.

- Repurchase of Stock (Buyback) – Companies can repurchase their own shares to reduce the number of shares outstanding. This is done to increase the stock price by reducing its market supply. This is also a cash outflow, as the company uses its cash reserves to buy back stock. Stock buybacks are often used to maintain stock levels or improve financial metrics.

- Issuance of Common Stock – This is the process through which a company issues new shares to raise additional capital. It may happen through public offerings or private investments. Issuing stock allows a company to acquire funds for business development, new projects, or debt repayments.

- Other Financing Activities – This category includes financial flows that don’t fall under the main financing activities, such as capital adjustments, debt repayments, or other non-listed expenses.

Summary Line: Net Cash Provided by (Used in) Financing Activities

This is the total of all financing activities. If this figure is positive, it indicates that the company raised more funds than it spent on financing (through stock issuance, debt obligations, or stock buybacks). If negative, it may indicate high debt repayments or significant dividend payouts.

Final Summary Line: Net Increase (Decrease) in Cash and Cash Equivalents

This is the final line, showing how much the company’s cash position has changed during the period. It’s the sum of all cash flows from operating, investing, and financing activities, giving the final change in the company’s cash holdings.

If the company has a positive net increase in cash, it suggests financial stability, as the company was able to increase its cash reserves. If negative, this could indicate liquidity issues, meaning the company may need additional financing or need to adjust its expenditure strategy.

Practical Application of Cash Flow Analysis

Cash Flow analysis is crucial for understanding how well a company manages its finances, generates cash, and makes investments. For instance, a company might show steady profit, but if its operating cash flow is negative, it could be in financial trouble, as it may not have enough cash to fund its activities despite its high income. Such an analysis gives a more realistic picture of the company’s financial health than just the income statement.

Importance for Investors:

Investors should closely monitor changes in the cash flow statement. Positive Cash Flow may indicate the company’s stability and ability to generate profits, which is crucial for potential investments or stock purchases. On the other hand, consistently negative cash flows could signal that the company may not meet its financial obligations or might be forced to reduce dividends.

Conclusion

When analyzing a company for investment, the cash flow statement can provide valuable insights into its ability to maintain stability, regardless of the profit it shows. Cash flow analysis, combined with other financial reports, helps build a comprehensive picture of the company's financial situation.