What is Quantitative Easing

What is Quantitative Easing?

Introduction

Following the global financial crisis of 2007–2008, a new term was introduced into economic theory and a corresponding monetary mechanism was implemented in practice: quantitative easing (abbreviated as QE). According to many experts, it was this very policy that saved the global economy from collapse. The world did not experience the same level of devastation brought by the Great Depression of 1929 and the subsequent economic recession.

QE was applied on an even larger scale (and continues to be applied at the time of writing) in many developed countries in response to a new financial crisis, unofficially dubbed the "coronacrisis," which was triggered by the stock market crash of February-March 2020. The world went into lockdown due to the spread of COVID-19, and the economy faced the threat of entering a prolonged recession (a period of decline with no growth).

To save global financial markets and prevent major corporations from going bankrupt, the European Union, the United States, and several other countries once again resorted to quantitative easing. It seems to have worked: consider the rebound of the index from its lowest point on March 23.

Chart: SPY Index

The results appear impressive. In less than three months, the S&P 500 index of the world's largest economy—the United States—reached nearly pre-crisis levels. Will this success last? Or is it just another attempt by politicians to save face before elections? We will try to address these and other questions in this article.

How Does Quantitative Easing Work?

Quantitative easing is the process of injecting liquidity into the economy by having the Central Bank (CB) purchase government bonds and other financial assets. The issuers of these bonds—whether governments or private companies—must repay their debts to the Central Bank or other holders over a specific period. The CB may also sell the accumulated financial assets later, withdrawing excess liquidity from the market.

According to modern economic theory, quantitative easing can only be effectively implemented in countries with low inflation and low interest (or policy) rates. Why does it work without causing inflation? Let’s refer to the Fisher Equation:

M*V=P*Q=GDP

Where:

- M: Money supply

- V: Velocity of money

- P: Price level

- Q: Production volume

During a crisis, VVV decreases because the economic activity of businesses slows, and households spend less and save more. As a result, turnover and company profits decline. Lower profits lead to cost optimization, which often means layoffs and, consequently, higher unemployment. Those who lose their jobs spend less, further reducing company revenues, increasing unemployment, and perpetuating this downward spiral. Ultimately, the economy faces recession, slow growth, or even depression—zero or negative growth.

To avoid this scenario, central banks increase MMM (as seen in the equation). These additional funds replace the temporarily withdrawn money, preventing the economy from declining (or mitigating the decline).

What Risks Does Quantitative Easing Pose?

Although the term "quantitative easing" appeared only in 2008, similar methods have been used in the economic policies of various countries in the past.

In 1932, under pressure from the U.S. Congress, the Federal Reserve purchased government bonds worth approximately $1 billion (when GDP, post-crash, was about $60 billion). In 2020 terms, this would be about $19 billion. However, this program was discontinued. At that time, the Fisher Equation had not yet been developed, and it was believed that low interest rates alone constituted sufficiently loose monetary policy.

Later, similar ideas appeared in economic textbooks and articles.

In the early 2000s, Japan attempted to use QE to combat deflation, but this approach was ultimately deemed ineffective, and the program was discontinued.

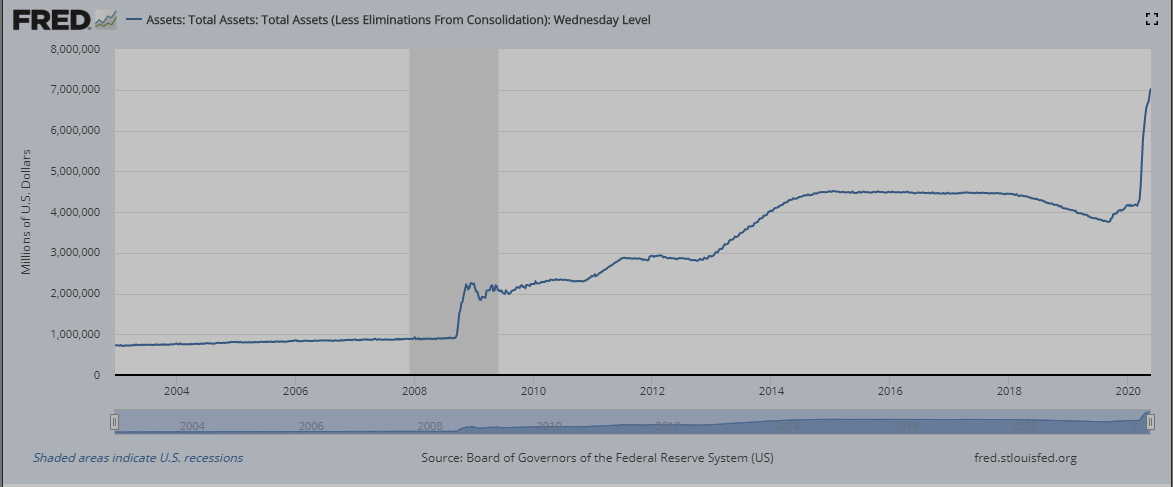

From 2008 to 2014, the U.S. conducted three large-scale rounds of quantitative easing, which many economists believe saved the U.S. economy from collapse. As shown in the chart, the Federal Reserve's balance sheet grew more than fourfold between 2008 and 2014.

Chart: Growth of the Federal Reserve’s Balance Sheet

During the 2007–2008 financial crisis, the UK, Switzerland, and the European Union also employed this tool, albeit on a smaller scale.

In 2020, the U.S. launched a new round of quantitative easing. As of June 1, 2020, the Federal Reserve’s balance sheet exceeded $7 trillion, meaning approximately $3 trillion was injected into the economy over three months—and this was far from the limit.

As shown in the first chart, the S&P 500 index rebounded from its low point, and, at least for now, there has been no significant inflation or devaluation of the U.S. dollar.

Chart: Euro-Dollar Exchange Rate

Conclusion

In summary, the risks of quantitative easing appear justified: it did not lead to runaway inflation, nor was there a sharp devaluation of the U.S. dollar. GDP experienced only a modest decline, and by 2009, economic growth resumed. Stock market indices in various industries reflected recovery.

Was this due to QE and the actions of central banks, or were there entirely different reasons behind overcoming the crisis?