Swarmer Q1 2026 Earnings Review

Artificial intelligence, autonomous systems, and defense technology have become some of the most closely watched investment themes in recent years. Companies operating at the intersection of these sectors have attracted significant investor attention, particularly as governments and private organizations increase spending on next-generation technologies.

Swarmer is one of the newest companies to emerge in this space. Following its high-profile Nasdaq debut earlier this year, the company quickly became a favorite among growth-oriented investors looking for exposure to autonomous drone software and AI-powered defense systems. However, with the excitement surrounding the stock came a new challenge: proving that its technology can translate into sustainable financial results.

The company's first quarterly earnings report as a public company offered investors their first real opportunity to evaluate that progress.

Why Investors Are Watching Swarmer

Swarmer operates in one of the fastest-growing segments of the defense technology market: autonomous drone coordination software.

Unlike traditional defense contractors that manufacture drones or hardware, Swarmer focuses on software. Its platform allows a single operator to coordinate large groups of autonomous systems simultaneously, effectively acting as the intelligence layer behind drone operations. According to the company, its software has already been used in more than 100,000 combat missions in Ukraine, providing real-world operational data that continuously improves its machine-learning models.

This distinction is important because software companies often have significantly higher scalability than hardware manufacturers. Once the platform is developed, each additional deployment can potentially generate revenue with relatively limited incremental costs.

Investors have also been drawn to the broader market opportunity. Military spending on autonomous systems continues to increase globally, while governments are looking for cost-effective technologies that can improve operational efficiency. As a result, companies that successfully position themselves as software providers for autonomous systems could benefit from a market that is expected to expand significantly over the next decade.

Key Takeaways from the Q1 2026 Report

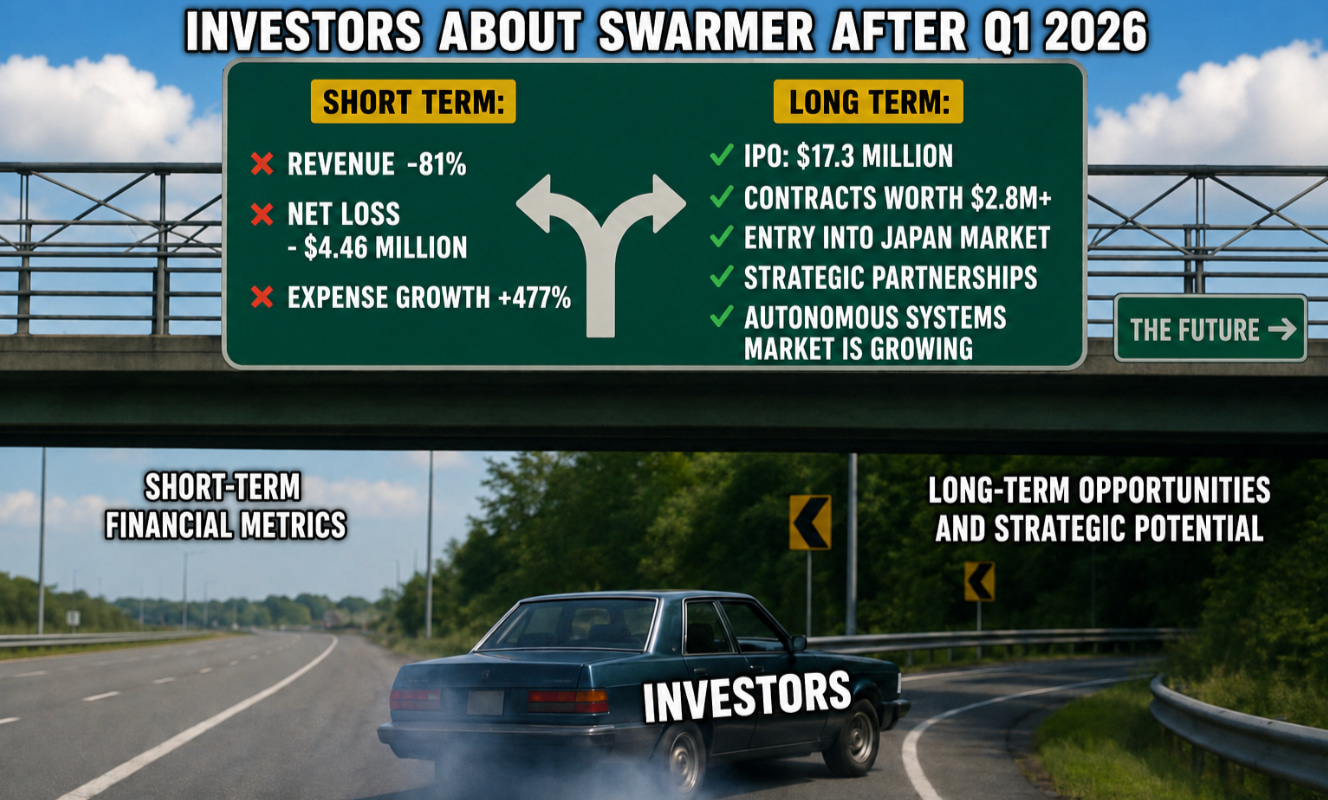

Swarmer's first-quarter results painted a mixed picture.

On one hand, the company reported revenue of just $20,325, a substantial decline from $110,704 in the same period last year. Gross profit turned into a gross loss, operating expenses increased sharply, and net losses widened considerably.

On the other hand, the report also highlighted several strategic developments that investors viewed positively:

A successful Nasdaq IPO that generated approximately $17.3 million in gross proceeds.

A $2.8 million software licensing contract covering more than 16,000 drone software licenses.

Expansion into Japan through cooperation with the Rakuten Group.

New technology partnerships aimed at strengthening communication resilience and counter-drone capabilities.

As a result, the market found itself balancing two competing narratives:

The financial results looked weak.

The strategic outlook looked promising.

And that tension remains at the center of the investment debate surrounding Swarmer.

Breaking Down the Numbers

Let's start with the headline figures.

*Compared to December 31, 2025.

The most obvious concern is revenue.

An 81% decline is significant under any circumstances. Management explained that the decrease was primarily due to the wind-down of deferred service revenue associated with what had historically been the company's largest customer in Ukraine. Importantly, management stated that it does not expect meaningful future revenue from this customer and is instead focusing on higher-volume opportunities both inside and outside Ukraine.

This explanation is critical because it suggests the decline may not necessarily reflect weakening demand. Instead, it may indicate a transition period as the company moves from one customer base toward a broader commercial strategy.

Still, investors will want to see evidence that new contracts can replace and eventually exceed the lost revenue.

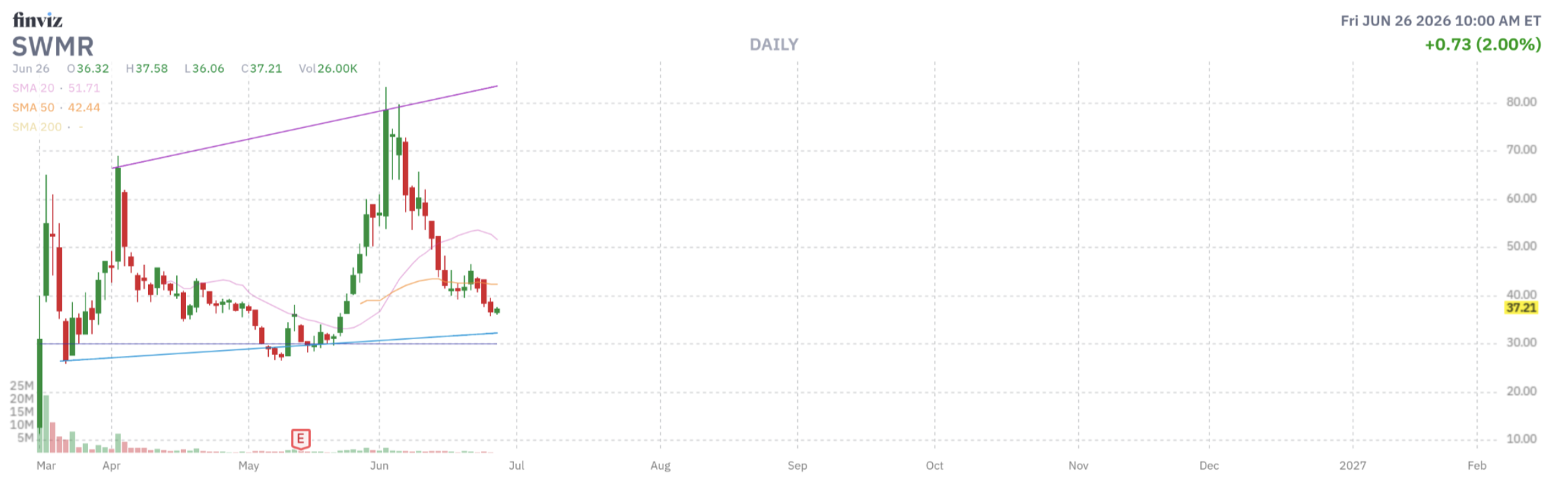

From a chart perspective, the stock is swinging within a very broad range, as expected for a recent IPO. With the parabolic peak on June 2, that level could remain the all-time high at least until the next quarterly earnings release.

Cash Position and Financial Health

For many early-stage technology companies, cash is often more important than earnings.

Swarmer ended the quarter with approximately $23.5 million in cash and cash equivalents, compared to $9.3 million at the end of 2025. The increase was largely driven by IPO proceeds and additional financing activity.

This matters because growth companies frequently operate at a loss while investing in:

engineering teams

product development

customer acquisition

strategic partnerships

The key question is whether those investments generate future growth.

At the current loss rate, investors will likely monitor cash burn carefully over the next several quarters. While the balance sheet appears significantly stronger following the IPO, the company must eventually demonstrate that increased spending is translating into meaningful commercial traction.

Contracts, Partnerships, and Growth Opportunities

Perhaps the most encouraging section of the report involved new business developments.

The company secured a $2.8 million software licensing contract covering more than 16,000 software licenses for SkyKnight drones and other UAV platforms.

In addition, subsequent announcements referenced agreements with potential value exceeding $13 million if future upgrade options are exercised.

Beyond direct contracts, management also highlighted several strategic initiatives:

Expansion into Japan with Rakuten support.

Partnership discussions involving resilient communications systems.

Development of a deployable drone interceptor platform.

These initiatives suggest management is attempting to diversify revenue sources while expanding internationally. For investors, this may ultimately prove more important than one weak quarter of revenue.

Conclusion

Swarmer's first quarterly report as a public company was neither a clear success nor a clear disappointment.

Financially, the numbers remain challenging. Revenue declined sharply, losses expanded, and investors still have limited visibility into the timing of future revenue growth.

Strategically, however, the story remains compelling. The company operates in one of the fastest-growing segments of the defense technology market, has secured meaningful contracts, strengthened its balance sheet through its IPO, and continues expanding partnerships across multiple regions.

For now, Swarmer remains a stock driven more by future expectations than current financial performance. The next several quarters will likely determine whether those expectations are justified. And for investors, that makes future earnings reports every bit as important as the technology itself.